The quality of a mortgage fund’s returns ultimately depends on the strength of its underwriting process. While many investors focus primarily on headline yield figures when evaluating funds, the underwriting methodology represents the critical foundation that determines both performance consistency and capital preservation. Understanding how sophisticated funds evaluate lending opportunities helps investors identify managers with the discipline and expertise necessary for long-term success.

Underwriting encompasses the comprehensive evaluation process that determines which loans enter a fund’s portfolio and under what terms. This multi-faceted assessment goes far beyond simple property valuation or borrower credit checks, incorporating numerous qualitative and quantitative factors that collectively determine risk profiles. The difference between exceptional and average mortgage funds often lies in the depth, consistency, and forward-looking nature of their underwriting approaches.

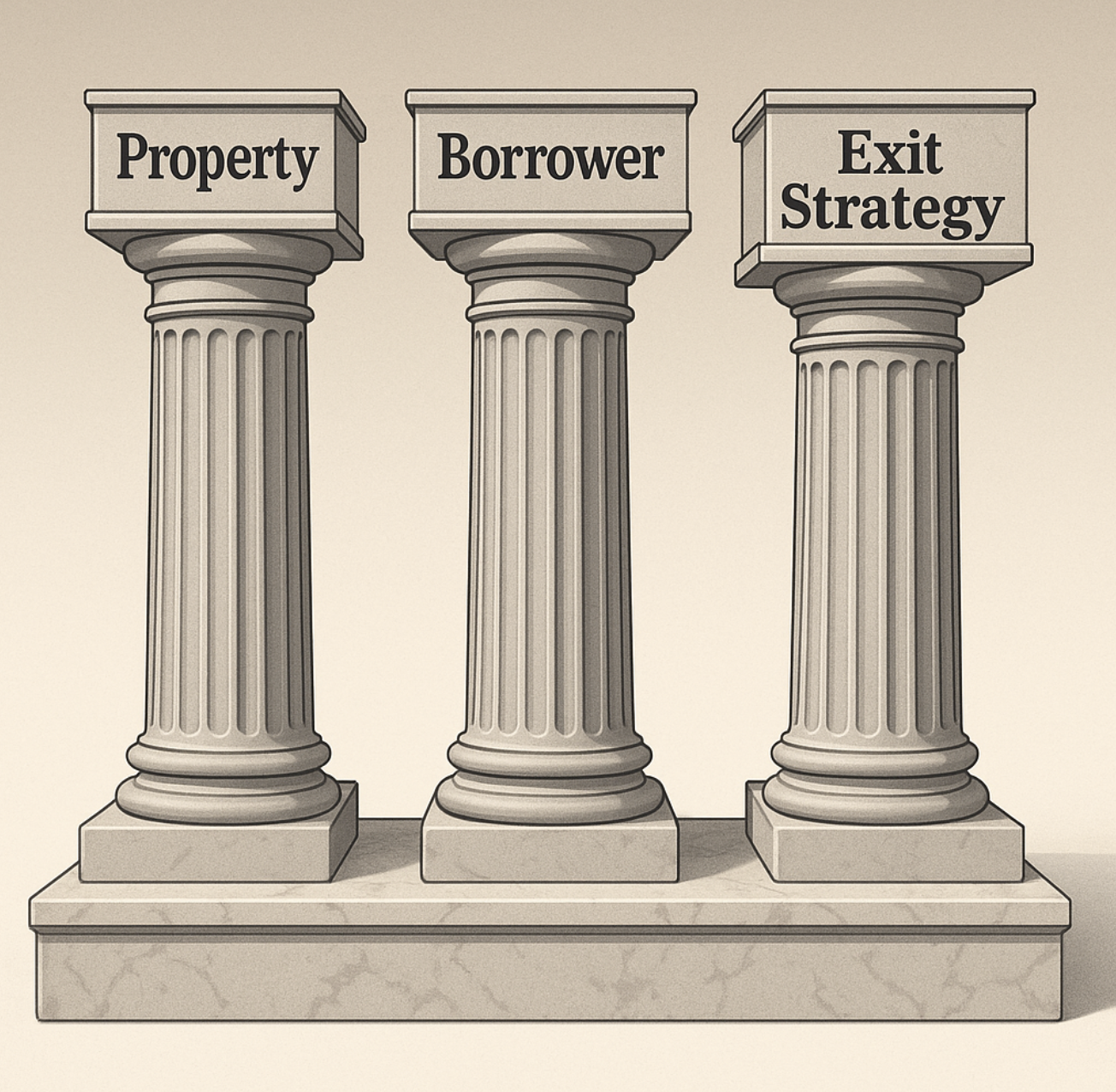

The Three Pillars of Comprehensive Underwriting

Sophisticated mortgage fund underwriting rests on three fundamental pillars:

Sophisticated mortgage fund underwriting rests on three fundamental pillars:

- Property assessment evaluates the fundamental collateral securing each loan, including current condition, location quality, market position, and potential challenges. This analysis forms the foundation of lending decisions, as the property ultimately represents the primary security for investor capital.

- Borrower evaluation examines the individuals or entities requesting financing, including their experience with similar projects, financial capacity, track record of execution, and relationship history. While private lending emphasizes property fundamentals over borrower metrics, borrower characteristics remain important secondary considerations.

- Exit strategy analysis focuses on how loans will ultimately be repaid, whether through property sale, refinancing with conventional lenders, or other means. This forward-looking assessment ensures loans have realistic repayment paths regardless of market conditions, creating multiple layers of protection for investor capital.

The Fidelis Private Fund Underwriting Approach

Fidelis Private Fund has developed a disciplined underwriting methodology designed to protect investor capital while maintaining attractive yields:

We employ a multi-layer approval process that incorporates diverse perspectives and expertise. This collaborative approach prevents individual biases from influencing decisions while ensuring all potential risks receive appropriate consideration before commitment.

Our underwriting emphasizes forward-looking analysis rather than merely evaluating current conditions. This perspective includes stress-testing potential loans under various market scenarios to ensure viability even if conditions deteriorate during the loan term.

We maintain consistent standards regardless of competitive pressures or market cycles. This disciplined approach prevents the common industry mistake of relaxing criteria during strong markets when competition increases, a pattern that often creates problems when conditions eventually normalize.

Property Underwriting: Beyond Basic Valuation

Comprehensive property assessment involves several critical components:

- Valuation methodology significantly impacts portfolio security, with conservative approaches providing greater protection than aggressive assumptions. Sophisticated funds typically employ multiple valuation techniques, including comparable sales analysis, income capitalization, and replacement cost considerations, to develop comprehensive property value assessments.

- Location quality analysis examines both current conditions and future trends affecting property marketability and value. This evaluation considers neighborhood characteristics, development patterns, employment drivers, and other factors that influence long-term property performance.

- Physical condition assessment identifies potential issues requiring attention while confirming property representations. This evaluation often includes professional inspections for larger loans, with particular focus on structural elements, deferred maintenance, and improvement needs that might impact value or marketability.

Borrower Underwriting: Experience and Capacity

While property fundamentals remain primary, borrower characteristics influence both risk profiles and execution probability:

- Experience relevance with similar projects provides important insights into execution capability. Successful underwriting evaluates not just general real estate background but specific experience with comparable property types, project scopes, and market conditions.

- Financial capacity beyond the specific project helps ensure borrowers can address unexpected challenges without default risk. While private lending focuses primarily on property collateral, borrower financial strength creates valuable risk mitigation that enhances overall security.

- Track record analysis examining previous project outcomes offers perhaps the most reliable predictor of future performance. This evaluation considers not just project completion but adherence to budgets, timelines, and quality standards across previous undertakings.

Exit Strategy Underwriting: The Critical Third Dimension

The most sophisticated aspect of mortgage fund underwriting focuses on loan repayment paths:

- Refinance exit analysis evaluates the probability of conventional takeout financing based on projected property performance, market conditions, and borrower qualifications. This assessment typically includes preliminary discussions with potential takeout lenders to confirm program availability and likely terms.

- Sales exit evaluation examines market absorption capacity, likely buyer pools, and projected pricing based on comparable properties. This analysis considers both current market conditions and potential future scenarios to ensure realistic exit assumptions.

- Contingency planning identifies alternative repayment strategies if primary exit paths encounter obstacles. This forward-looking approach ensures loans have multiple potential resolution paths rather than depending on single-scenario outcomes.

Risk-Based Pricing: Aligning Returns with Risk Profiles

Beyond approval decisions, underwriting determines appropriate loan terms based on risk assessment:

Beyond approval decisions, underwriting determines appropriate loan terms based on risk assessment:

- Interest rate determination follows risk-based pricing models that align returns with specific risk profiles. This calibration ensures the fund receives appropriate compensation for the particular risks associated with each loan rather than applying standardized pricing.

- Loan-to-value adjustments based on property type, location quality, borrower strength, and market conditions create appropriate equity cushions for each specific opportunity. These adjustments ensure protection layers correspond to the particular risk characteristics of individual loans.

- Fee structures including origination points, extension fees, and other charges complement interest returns while creating appropriate incentives for timely repayment. These structures help align borrower and lender interests while enhancing overall fund yields.

Technology and Human Judgment: The Optimal Balance

Modern mortgage fund underwriting combines technological tools with experienced human assessment:

- Data analytics enhance decision quality by identifying patterns, correlations, and potential concerns that might not be immediately apparent through traditional analysis. These tools help quantify risks while providing objective metrics that complement subjective evaluations.

- Market intelligence platforms provide real-time information about comparable properties, transaction trends, and economic indicators that influence lending decisions. These resources enhance underwriting accuracy while ensuring decisions reflect current market realities.

- Human judgment remains irreplaceable for evaluating qualitative factors, recognizing unique opportunities, and identifying potential concerns that automated systems might miss. The most effective underwriting combines technological efficiency with experienced human oversight that contextualizes analytical findings.

Underwriting Evolution Through Market Cycles

Sophisticated funds adjust underwriting approaches based on market conditions while maintaining core principles:

- Late-cycle conservatism typically emerges as experienced managers recognize increasing market frothiness. These adjustments often include reduced loan-to-value ratios, increased debt service coverage requirements, and greater scrutiny of exit strategies as markets approach potential inflection points.

- Opportunity recognition during market corrections allows disciplined funds to secure exceptional loans when competition decreases. Funds that maintained conservative standards during boom periods typically have both the capital and confidence to provide solutions when markets normalize.

- Consistent core principles regardless of market conditions distinguish truly professional underwriting from approaches that fluctuate with market sentiment. While specific parameters may adjust, fundamental requirements for property quality, borrower capability, and exit viability remain constant.

Investor Due Diligence: Evaluating Underwriting Quality

When assessing mortgage funds, several underwriting-related factors merit particular attention:

- Underwriting transparency regarding methodology, approval processes, and risk assessment provides crucial insights into fund quality. Managers willing to discuss their approaches in detail, including specific examples of declined opportunities, typically demonstrate the discipline that enhances long-term performance.

- Team experience through multiple market cycles offers valuable perspective that purely analytical approaches cannot provide. Underwriters who have witnessed previous market corrections typically incorporate those lessons into current decision-making, creating more resilient portfolios.

- Track record analysis examining historical loan performance provides perhaps the most reliable indicator of underwriting quality. Funds with minimal defaults and losses through various market conditions typically demonstrate the underwriting discipline necessary for continued success.

For investors seeking stable income with strong capital preservation, Fidelis Private Fund offers a professionally managed mortgage fund with disciplined underwriting designed to protect investor capital while delivering attractive yields. Contact us today at 760-258-4486 to learn more about our investment approach and current opportunities.

Explore how Fidelis can support your growth with flexible, fast financing solutions tailored to your needs.

See Our Latest Performance Report

Fidelis Private Fund annualized yield paid to Limited Partners for the 1st Quarter 2025. Click here for a summary of Fidelis’s annualized yield since inception.

Fidelis Private Fund annualized yield paid to Limited Partners for the 1st Quarter 2025. Click here for a summary of Fidelis’s annualized yield since inception.

Fidelis 2028 Vivid Vision – Where are we going and how are we going to get there!

Fidelis 2028 Vivid Vision – Where are we going and how are we going to get there!

The Fidelis 2028 Vivid Vision document provides a comprehensive blueprint of the company’s strategic direction, core values, and operational principles, highlighting its commitment to capital preservation, growth, innovation, and client-centric services. Click to read the Fidelis vision.