There is a specific kind of “knot in the stomach” that many of my investors describe when we sit down to talk. It isn’t the fear of a sudden market crash—most of the people I partner with have the resilience to weather a storm. Rather, it is the quiet, persistent anxiety caused by inflation. It’s the realization that while your account balance might be holding steady, the actual purchasing power of that capital is being slowly eroded.

In the world of fixed income, this fear is well-founded. If you are locked into a long-term instrument while the cost of living—and the cost of capital—climbs, you aren’t just standing still; you are falling behind.

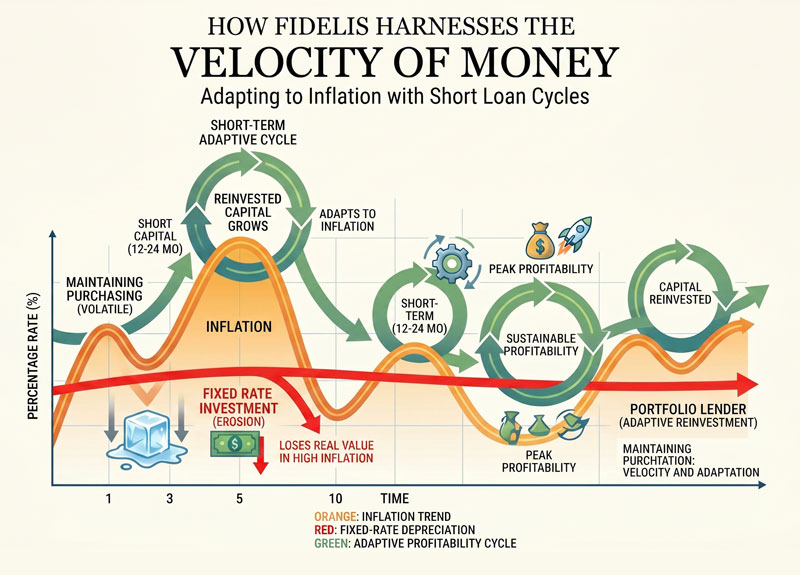

As a steward of your capital, my primary role is Capital Preservation. I view myself first as a protector of what you have built, and second as a generator of yield. To protect wealth in an inflationary environment, we have to look at a concept often overlooked in the private debt space: the Velocity of Money.

The Trap of the Long Horizon

Most investors think of “safety” in terms of duration. They look for 10-year or 20-year horizons, thinking the length of the commitment equates to the stability of the return. However, in an inflationary cycle, duration is often the enemy. When you lock capital into a long-term fixed rate, you lose the ability to adapt. You are stuck with yesterday’s pricing in tomorrow’s economy.

Most investors think of “safety” in terms of duration. They look for 10-year or 20-year horizons, thinking the length of the commitment equates to the stability of the return. However, in an inflationary cycle, duration is often the enemy. When you lock capital into a long-term fixed rate, you lose the ability to adapt. You are stuck with yesterday’s pricing in tomorrow’s economy.

The alternative is to seek out investments that “re-price” frequently. This is where the short-term mortgage fund model becomes a powerful tool for maintaining purchasing power.

Understanding Re-Pricing Frequency

At Fidelis Private Fund, we focus on short-term bridge loans, typically with a maturity of 12 to 24 months. By keeping the loan duration short, we ensure that a significant portion of the fund’s capital is returning to us every few months. This is the “Velocity of Money” in action.

As these loans pay off, that capital is “re-born.” We are then able to reinvest it—or re-price it—at current market rates. If inflation has driven interest rates higher, the fund naturally adjusts. We aren’t stuck holding a low-yield note from three years ago; we are originating new notes that reflect the reality of today’s market. This inherent agility acts as a natural hedge, ensuring the yield we generate for our investors isn’t swallowed by the rising cost of goods.

The Fidelis Way: Precision in Stewardship

To execute this strategy effectively, the “how” matters as much as the “why.” Our approach is Relationship-Driven, but our operations are built on precision.

Every loan in our portfolio is originated and underwritten directly by us. This is a critical distinction. We do not outsource the decision-making. We personally evaluate the borrower, the asset, and the exit strategy to ensure it meets our standards for Stewardship. We are the ones looking at the property, analyzing the equity cushions, and making the hard “yes” or “no” calls.

However, once a loan is funded, we believe in using specialized experts for the administrative heavy lifting. While we make all the underwriting and investment decisions, our loans are serviced by a trusted, professional third-party loan servicer. This ensures that the technical aspects of payment processing, tax reporting, and payoff demands are handled with institutional-grade accuracy, allowing our team to stay focused on what we do best: protecting your capital and finding the next high-quality opportunity.

Moving Beyond the “Fixed” Mindset

Moving Beyond the “Fixed” Mindset

Fixed income doesn’t have to mean “stagnant income.” By shortening the duration of the underlying assets, we transform a portfolio from a static snapshot into a living, breathing entity that can move in tandem with the economy.

My goal has always been to provide our investors with more than just a check; I want to provide the peace of mind that comes from knowing your capital is being actively managed by someone who views your investment as a sacred trust. We aren’t just looking for yield; we are looking for the smartest way to ensure that your wealth today buys just as much—if not more—tomorrow.

I’ve always believed that the best way to build a partnership is through direct communication. I don’t believe in gatekeepers or corporate layers. If you have questions about how we are positioning the fund for the current year, or if you just want to talk through your own investment goals, the best way to start is just to reach out. I answer my own phone, and I’d truly love to hear your story.

You can reach me directly at 760-258-4486, or send me an email at jlloyd@fidelispf.com. Let’s discuss how we can protect what you’ve worked so hard to build.

See Our Latest Performance Report

Fidelis Private Fund annualized yield paid to Limited Partners for the 4th Quarter 2025. Click here for a summary of Fidelis’s annualized yield since inception.

Fidelis Private Fund annualized yield paid to Limited Partners for the 4th Quarter 2025. Click here for a summary of Fidelis’s annualized yield since inception.

Fidelis 2028 Vivid Vision – Where are we going and how are we going to get there!

Fidelis 2028 Vivid Vision – Where are we going and how are we going to get there!

The Fidelis 2028 Vivid Vision document provides a comprehensive blueprint of the company’s strategic direction, core values, and operational principles, highlighting its commitment to capital preservation, growth, innovation, and client-centric services. Click to read the Fidelis vision.